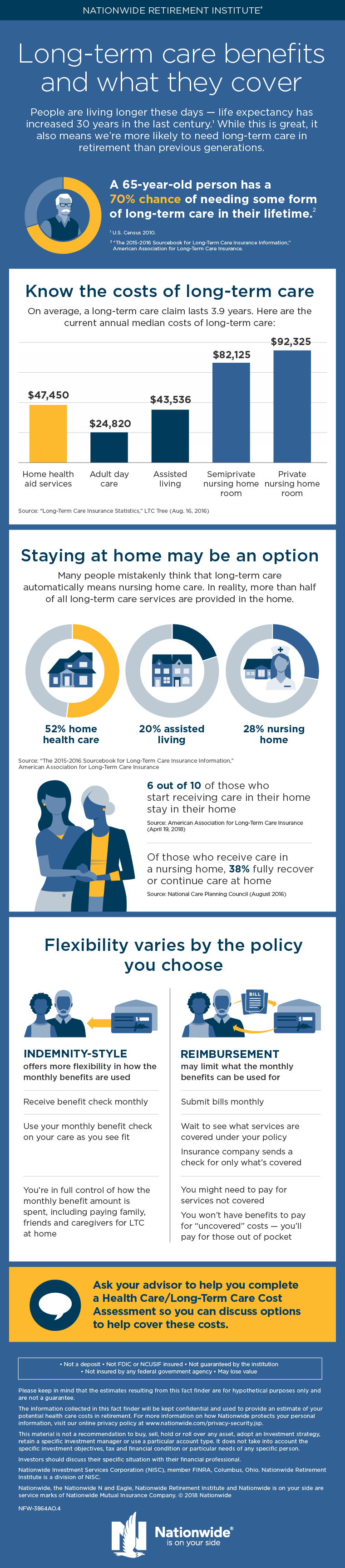

Long Term Care benefits and what they cover

Call us today for a free quote...

San Francisco Corporate HQ:

(Monday - Friday @10am - 4pm)

1550 Noriega St. Suite 100, SF CA 94122

San Jose Branch: (by appointment)

4320 Stevens Creek Blvd. Suite 191

Fremont Branch: (Tues/Thur)

42808 Christy St. Suite 112

Oakland Branch: (by appointment)

638 Webster St. Suite 420

Tel: 1-888-746-6688

415-661-3885

contact us

Medicare - Enroll now

© eHealth-Plans Inc. / Amazing Wealth Insurance Agency 1989-2024 This website is designed to provide general information. It is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market or recommend any tax plan. Please note Simon Chew, CIC and his team of agents do not give legal or tax advice.